Navigating the Maze: A Comprehensive Guide to Housing Loan Eligibility in Singapore

Homeownership in Singapore is more than just a dream; it’s a deeply ingrained aspiration, a cornerstone of financial security, and a significant life milestone for many. However, with property prices steadily climbing and the financial landscape becoming increasingly complex, securing a housing loan is a meticulous process that requires a thorough understanding of eligibility criteria. This article aims to demystify the intricacies of housing loan eligibility in Singapore, providing a comprehensive guide for prospective homeowners to navigate the requirements for both public (HDB) and private properties.

The Dual Housing Market: HDB vs. Private Property Loans

Singapore’s housing market is distinctly divided into two primary segments: public housing managed by the Housing & Development Board (HDB) and private properties. The eligibility criteria for purchasing a property and, consequently, for obtaining a housing loan, differ significantly between these two segments. Understanding this fundamental distinction is the first step towards securing your dream home.

For HDB flats, buyers typically have two loan options: the HDB Housing Loan (offered directly by HDB) or a bank loan (offered by commercial banks). For private properties, only bank loans are available. Each option comes with its own set of rules, regulations, and financial considerations.

I. HDB Housing Loan Eligibility: The Public Housing Pathway

The HDB Housing Loan is often the preferred choice for first-time HDB flat buyers due to its more stable interest rates and higher Loan-to-Value (LTV) limits compared to bank loans for HDB properties. However, eligibility is stringent and designed to support Singaporean citizens in acquiring public housing.

A. General Eligibility to Purchase an HDB Flat (Prerequisite for HDB Loan):

Before even considering the loan, applicants must first meet the general criteria to purchase an HDB flat:

- Citizenship: At least one applicant must be a Singapore Citizen (SC). If a couple, one must be an SC and the other a Singapore Permanent Resident (SPR), or both must be SCs.

- Age: At least 21 years old at the time of application. For singles buying under the Single Singapore Citizen Scheme, they must be 35 years old and above.

- Family Nucleus: Applicants must form a proper family nucleus (e.g., married couple, fiancé/fiancée, parent(s) with child(ren), siblings) or qualify under specific schemes like the Single Singapore Citizen Scheme.

- Income Ceiling: The monthly household income must not exceed the prevailing income ceiling (currently S$14,000 for families, S$21,000 for extended families, and S$7,000 for singles buying 2-room Flexi flats). This ceiling ensures that HDB flats remain accessible to middle and lower-income households.

- Property Ownership: Applicants must not own any other property (HDB flat, private residential property, or commercial property, both locally or overseas) at the time of application. Even if they have previously owned private property, they must dispose of it at least 30 months before applying for an HDB flat.

B. Specific Eligibility for HDB Housing Loan:

Even if you meet the general criteria to buy an HDB flat, additional conditions apply for the HDB Housing Loan:

- Citizenship & Age: Same as above.

- Income Ceiling for Loan: This is distinct from the flat purchase income ceiling. For HDB loans, the income ceiling is currently S$14,000 for families and S$7,000 for singles. If your income exceeds this, you will need to take a bank loan.

- No Private Property: You must not own any private property (local or overseas) at the point of application for the HDB Housing Loan. If you previously owned private property, you must have disposed of it for at least 30 months prior to applying for the HDB loan. This restriction is crucial and often overlooked.

- No Outstanding HDB Loans: You must not have taken two or more HDB housing loans previously. The HDB loan is generally limited to two times to ensure fair access.

- Creditworthiness: HDB will assess your financial standing, employment history, and existing debt commitments to determine your ability to service the loan. While HDB’s assessment may be less rigorous than banks, a history of poor credit or excessive debt can still affect approval.

- Loan-to-Value (LTV) Limit: The maximum LTV for an HDB Housing Loan is 85% (previously 90%, adjusted in December 2021). This means you must fund the remaining 15% with cash and/or CPF Ordinary Account (OA) savings.

- Loan Tenure: The maximum loan tenure is 25 years or up to the borrower’s age of 65, whichever is shorter.

C. Impact of CPF Usage and Grants:

HDB flat buyers can utilize their CPF Ordinary Account (OA) savings for the down payment and monthly loan repayments. Various HDB grants (e.g., Enhanced CPF Housing Grant, Proximity Housing Grant) can significantly reduce the cash outlay and overall loan amount, improving affordability. Eligibility for these grants also has its own set of criteria, primarily linked to income, citizenship, and proximity to parents.

II. Bank Loan Eligibility: For HDB and Private Properties

Bank loans are available for both HDB and private properties and are subject to the regulations set by the Monetary Authority of Singapore (MAS). Unlike HDB loans, bank loans typically offer more flexibility in terms of interest rate packages (fixed, floating, SORA-pegged) but come with stricter affordability frameworks.

A. General Requirements for Bank Loans:

- Citizenship: Open to Singapore Citizens, Permanent Residents, and foreigners. However, LTV limits and stamp duties differ based on citizenship status.

- Age: Typically between 21 and 65-75 years old. The maximum loan tenure will be capped based on the borrower’s age.

- Income: Stable and verifiable income is paramount. Banks assess your ability to make monthly repayments. This includes:

- Salaried Employees: Payslips (past 3-6 months), CPF statements (past 12 months), income tax assessments.

- Self-Employed: Income tax assessments (past 2-3 years), company financial statements, bank statements. Banks often "haircut" self-employed income (e.g., take 70% of declared income) for a more conservative assessment.

- Commission-Based/Variable Income: Banks usually take an average of 6-12 months of income.

- Credit Score: Your credit report from the Credit Bureau Singapore (CBS) is crucial. Banks look for a healthy credit score, indicating responsible management of past and present debts (credit cards, personal loans, car loans). A low score or history of defaults will significantly impact loan approval.

- Employment Stability: Banks prefer borrowers with stable employment histories. Frequent job changes or periods of unemployment can raise red flags.

B. Key Regulatory Frameworks Governing Bank Loans:

These regulations are critical for determining the maximum loan amount you can obtain.

-

Total Debt Servicing Ratio (TDSR):

- Purpose: Introduced by MAS, TDSR ensures that borrowers do not over-leverage themselves. It caps the percentage of a borrower’s gross monthly income that can be used to service all debts.

- Limit: Currently set at 55%. This means your total monthly debt obligations (including the new housing loan, car loans, personal loans, credit card debts, study loans, etc.) cannot exceed 55% of your gross monthly income.

- Calculation:

- For fixed income, 100% of gross income is used.

- For variable income (e.g., commission, bonus, rental income, self-employed income), only 60% of the variable component is typically counted.

- A stress test interest rate (e.g., 3.5% for residential properties) is used to calculate the new housing loan’s monthly repayment, even if the actual market rate is lower. This builds a buffer against future interest rate hikes.

- Example: If your gross monthly income is S$10,000, your total monthly debt repayments cannot exceed S$5,500. If you have existing debts of S$2,000/month, your new housing loan repayment (calculated at the stress test rate) cannot exceed S$3,500.

-

Mortgage Servicing Ratio (MSR):

- Purpose: This regulation applies specifically to loans for HDB flats and Executive Condominiums (ECs) purchased directly from the developer. It further restricts the portion of income that can be used for housing loan repayments.

- Limit: Currently set at 30%. This means your monthly repayments for the HDB/EC housing loan (calculated using a stress test interest rate) cannot exceed 30% of your gross monthly income.

- Impact: If you are buying an HDB flat or new EC with a bank loan, you must satisfy both the TDSR and MSR rules. The MSR is generally the more restrictive of the two for these property types.

-

Loan-to-Value (LTV) Limits:

- Purpose: LTV dictates the maximum percentage of the property’s valuation or purchase price (whichever is lower) that a bank can lend. The remaining portion must be paid via cash and/or CPF OA.

- Factors Affecting LTV:

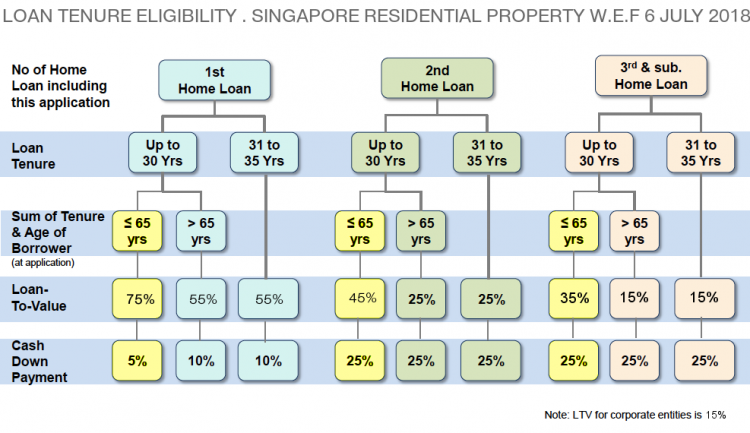

- Number of Existing Housing Loans:

- First Housing Loan: Max LTV is 75%. The remaining 25% must be paid, with at least 5% in cash and the rest (up to 20%) from CPF OA.

- Second Housing Loan: Max LTV is 45% (if the loan tenure extends beyond the borrower’s age of 65 or the loan period exceeds 30 years) or 55% (if not). At least 25% must be in cash.

- Third and Subsequent Housing Loans: Max LTV is 35% (if tenure/age limits exceeded) or 45% (if not). At least 25% must be in cash.

- Loan Tenure: If the loan tenure exceeds 30 years (or 25 years for HDB flats) or extends past the borrower’s age of 65, the LTV limits are reduced.

- Borrower’s Age: The LTV limits are generally lower for older borrowers, as the loan tenure would be shorter.

- Number of Existing Housing Loans:

- Example: For a S$1,000,000 first property, the maximum loan is S$750,000. You need to pay S$50,000 in cash and can use up to S$200,000 from CPF OA.

C. Other Factors Affecting Bank Loan Eligibility:

- CPF Usage: Similar to HDB loans, CPF OA can be used for down payments and monthly instalments, subject to CPF withdrawal limits (Valuation Limit and Withdrawal Limit).

- Property Type: Some banks may have preferences or stricter criteria for certain property types (e.g., very old leasehold properties, properties with unique features, shoebox units).

- Valuation: Banks will conduct their own valuation of the property. The loan amount is based on the lower of the purchase price or the bank’s valuation. If the valuation is lower than the purchase price, you will need to pay the difference in cash (the "cash over valuation" or COV).

III. Key Factors Influencing Approval and Loan Terms

Beyond the regulatory frameworks, several practical aspects significantly influence a bank’s decision and the terms of your loan.

-

Income Stability and Verification:

- Employment Type: Salaried employees with stable roles are generally seen as lower risk. Self-employed individuals, freelancers, or those with highly variable income (e.g., high commission) may face more scrutiny and potentially lower loan quantum or higher interest rates.

- Required Documents: Banks will request a comprehensive set of documents, including payslips, employment letters, CPF contribution statements, income tax returns (NOA), and bank statements to verify income and financial standing.

-

Age and Loan Tenure:

- The maximum age at which a loan can be fully repaid (typically 65 or 75, depending on the bank and policy) directly affects the maximum loan tenure. A shorter tenure means higher monthly repayments, impacting TDSR/MSR.

- For joint borrowers, banks typically use the income-weighted average age or the age of the youngest borrower for tenure calculations.

-

Financial Health Beyond TDSR/MSR:

- While TDSR and MSR set the legal limits, banks also look at your overall financial prudence.

- Savings and Assets: Having substantial savings, investments, or other liquid assets demonstrates financial resilience.

- Existing Debt Profile: Even if within TDSR, a high number of small debts can be viewed negatively. Banks prefer borrowers with manageable debt-to-income ratios.

- Dependents: While not directly factored into TDSR, a large number of dependents might indirectly influence a bank’s assessment of disposable income.

-

Credit History and Score:

- A clean credit record (no missed payments, defaults, or bankruptcies) is vital.

- Banks access your credit report to assess your payment behaviour, credit utilization, and the types of credit facilities you hold.

- It’s advisable to check your own credit report annually to ensure accuracy and address any issues.

-

Property Specifics:

- The type of property (e.g., residential, commercial, industrial), its age, remaining lease, and location can influence a bank’s willingness to lend and the LTV offered.

- Properties with very short remaining leases (e.g., less than 60 years) may face reduced LTVs or even be unmortgageable by some banks.

IV. The Application Process and What to Expect

The journey to securing a housing loan typically involves several steps:

- In-Principle Approval (IPA) / Approval-in-Principle (AIP): This is a crucial first step. Before committing to a property, get an IPA from a bank. It’s a conditional approval that states how much the bank is willing to lend you based on your financial profile. This helps you understand your budget and streamlines the actual loan application once you’ve found a property.

- Loan Application: Once you’ve identified a property, you formally apply for the loan with your chosen bank. You’ll submit all required documents.

- Valuation: The bank will arrange for an independent valuer to assess the property’s market value.

- Offer Letter: If approved, the bank issues a Letter of Offer, detailing the loan amount, interest rates, tenure, and terms and conditions.

- Acceptance and Legal Process: You accept the offer, and the bank’s appointed lawyers (or your own) will handle the legal documentation, including the mortgage agreement.

- Disbursement: Upon completion of the legal process and meeting all conditions, the loan amount is disbursed.

V. Common Pitfalls and How to Prepare

- Underestimating All-Inclusive Costs: Beyond the property price, factor in Buyer’s Stamp Duty (BSD), Additional Buyer’s Stamp Duty (ABSD – for PRs, foreigners, or multiple property owners), legal fees, valuation fees, agent fees, and renovation costs.

- Poor Credit Score: Address any outstanding debts or missed payments before applying for a loan. Pay bills on time and avoid excessive credit card utilization.

- Unstable Income: If you have variable income, ensure you have sufficient savings to cover potential shortfalls and maintain a consistent financial record for at least 6-12 months.

- Not Understanding Regulations: Many borrowers are caught off guard by TDSR, MSR, or LTV limits. Engage with a mortgage broker or bank representative early to understand your exact eligibility.

- Lack of Financial Planning: Without a clear budget and understanding of your financial limits, you risk over-leveraging or not being able to afford your desired property.

- Not Comparing Loan Packages: Interest rates and terms vary significantly between banks. Compare different packages and understand the lock-in periods, penalty clauses, and conversion options.

Conclusion

Navigating housing loan eligibility in Singapore is a journey that demands meticulous planning, diligent research, and a clear understanding of the regulatory landscape. Whether you are aiming for an HDB flat or a private condominium, the rules governing your eligibility for a loan are designed to ensure financial prudence and a stable housing market.

By thoroughly understanding the distinctions between HDB and bank loan criteria, the crucial role of TDSR, MSR, and LTV limits, and diligently preparing your financial profile, you can significantly enhance your chances of securing the necessary financing. Always remember to get an In-Principle Approval before committing to a property and consider seeking advice from qualified financial advisors or mortgage specialists to tailor a solution that best fits your unique circumstances. With careful preparation, the dream of homeownership in Singapore can become a tangible reality.